George Square Financial Management - Interest Rate Update

In response to The Bank of England interest rate increase I thought an update on the current financial situation may be useful.

The big 5.0: UK Interest rates jump as inflation bites.

Last week The Bank of England surprised financial markets by raising interest rates to 5%, a jump of 0.5% which is sharper than most had expected.

The decision comes in response to a surprise inflation number earlier in the week that showed the rising cost of living staying at 8.7% in June, rather than falling to 8.4% as had been expected. Worryingly both wages and goods were rising together.

Why has the Bank of England moved so aggressively?

Central Banks, including our own Bank of England, raised interest rates to suppress demand in the economy and bring down inflation. Their primary goal is to keep prices stable because when they are not it can create the very difficult situation of falling economic growth and rising prices. Such a situation when it becomes entrenched is the most significant kind of economic problem - creating hardship that can last for years.

So far, the Bank of England’s efforts to curb our inflation have proved less effective than others around the world. It is trusting that shock and awe might have more affect and also re-gain the confidence of financial markets who must believe they have what it takes to get the job done.

Why is the situation worse in the UK than in other countries?

In most major economies including the largest, the United States, inflation is falling fast. This enabled their Central Bank to pause interest rate rises in June and hint that there may only be one or two more before the job is done.

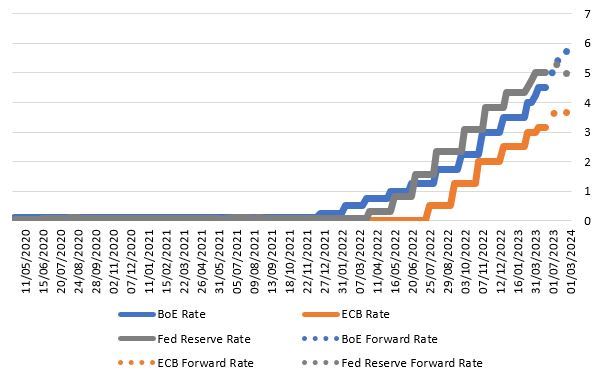

Investors are increasingly confident that a full-blown recession there can be avoided and those companies most sensitive to inflation increases are on the rise again. Here in the UK though times are much tougher. This means that the market is betting our interest rates will carry on rising even as others come down, which is shown in the graph below.

Source: Bloomberg, 20/04/2020 to 14/06/2023

So why is it so much worse for us? This is a difficult question because it strays into political views for many people. Part of the answer is surely that the Bank of England did not act fast enough initially, and action taken too late is simply less effective than action taken early.

However, there are more controversial reasons. Firstly, we were particularly vulnerable to higher natural gas prices in the first phase of the war in the Ukraine as a result of the energy importing, we undertake. In the United States for example the idea of energy independence has been agreed by all parties for decades and this insulated them. However, secondly most independent analysts agree that it is easier for both the Eurozone and the United States to cope with inflation in things like food prices because they are part of big single markets. Labour costs can diffuse across the region and goods can be moved free of tariffs to where they are needed. This forces down prices. Post Brexit we do not have this luxury in the United Kingdom, and this has made us vulnerable. We have also lost access to the European workers who helped control wage inflation in the United Kingdom.

When will inflation come down?

There are early signs that inflation is now falling with supermarkets for example reporting food price rises easing for the first time in more than a year. Some of our inflation is imported and linked to the price of raw materials and energy and this is falling. However, there is a very long way to go. It now seems likely that a recession is the price that must be paid to remove this inflationary pressure from the system. Whilst we can expect it to ease as the year goes on, it may be a number of years until it is fully resolved.

Does this mean a recession?

It is our view that the UK will enter a recession as a result of high interest rates and high inflation. However, we should not anticipate it to be a recession on a par with that seen during the Covid pandemic or after the Global Financial Crisis. Once the recession bites and domestic inflation pressure recedes, the Bank of England will be keen to rapidly reduce the cost of money and boost our flagging economy.

What can the Government do?

The hard truth here is not very much. There will be calls for action to help those with mortgages that are seeing rapidly rising interest payments. However, if the government were to cap those interest rate rises the Bank of England would likely not see the impact on inflation that it is seeking. It is likely instead that it will simply prevent any repossessions occurring for those who fall foul of higher interest rates. However, expect this decision to be taken all too slowly for those consumed by the worry of this situation. Other than that, the stark reality is that Prime Minister Rishi Sunak does not have any bright ideas and we should not deceive ourselves that there is an obvious alternative plan from Labour. The only sure-fire way to get down inflation is to raise interest rates, take the pain from those rises and wait. The best Governments can do is to try to insulate the most vulnerable from that pain without working against the Central Bank – a tough ask.

What does this mean for my portfolio?

The problems in the UK mean less than you might think for your portfolio. We invest using a globally diversified approach. This means that even when there is trouble in our home market, we can find opportunities overseas. It is also mistaken to assume that problems in our economy necessarily translate directly to our Stock Market which has very large exposure overseas itself. One significant area is whether this crisis forces the price of government bonds (gilts) down further. We think that gilts are already pricing in some pretty bad news and that ultimately, they will offer an opportunity for investors.

Now bank accounts offer a good interest rate should I just own cash?

There are two key reasons why ditching your portfolio in favour of cash may be a poor decision at the current time, even though bank interest rates now look at first glance more attractive.

- 1. The return on cash has not really gone up. Every investment we make must keep pace with inflation if it is to hold its value for us in future. A cash rate of 5% when inflation is at close to 9% is effectively losing 4% of its buying power each year. Your money is falling in terms of the true value it gives you in your life, even if you don’t see the number going down. By contrast, diversified investments in shares, bond and other assets have been shown over the long-term to be the only repeatable way to beat inflation and grow your buying power. The price investors pay for this is some volatility. The inflation will not be matched each and every year but is over the long-term.

- 2. The best returns are often made during and just after recessions. One of the challenges of trying to time when to invest in the Stock Market is that most often the best returns are actually made during recessions, and sometimes just after them. As soon as financial markets understand how bad a recession will be they ‘put it in the price’. Soon after this, recoveries can come fast, even though the real economy is still in trouble. Attempting to keep your money in cash and wait for a recovery often means you are missing this most beneficial time to be invested. Worse than that, those assets in cash will have fallen in terms of their buying power and then missed out on the returns that can re-capture it.

We believe the soundest response, notwithstanding the individual circumstances, is to stay invested through difficult times and trust that over the long-term, problems do get solved. Interest rate rises are painful, but they are healing for the global economy. Ultimately, they drive inflation out of the system and allow the economy to re-build.

The value of investments, and the income from them, can go down and you may get back less than invested. Changes in currency exchange rates may affect the value of your investment. This material may include charts displaying financial instruments' past performance as well as estimates and forecasts. Past performance is not an indicator of future returns. Capital at risk.

All Rights Reserved The content of this material is a marketing communication, and not independent investment research. As such, the legal and regulatory requirements in relation to independent investment research do not apply to this material and it is not subject to any prohibition on dealing ahead of its dissemination. The material is for general information purposes only (whether or not it states any opinions). It does not consider your personal circumstances or objectives. Nothing in this material is (or should be considered to be) legal, financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by George Square FM that any particular investment, security, transaction, or investment strategy is suitable for any specific person. Although the information set out in this marketing communication is obtained from sources believed to be reliable, George Square FM makes no guarantee as to its accuracy or completeness. George Square FM shall not be responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

George Square FM is authorised and regulated by the Financial Conduct Authority