George Square Commentary – August 2023 In conjunction with Albemarle Street Partners

More interest rate pain but economic clouds slowly disperse

The heat of the Summer brought more pain for borrowers, with both the US Federal Reserve and the Bank of England hiking interest rates further to tackle inflation. Yet to some extent the economic storm clouds are dispersing. In the United States, by far the world’s largest economy, the efforts to drive away inflation look to have been successful. Inflation stands at 3% now, lower than anyone had anticipated. Here in the United Kingdom, whilst we look sharply worse than the rest of the world, our inflation is starting to fall too.

All of this means that the risk of a significant global recession is receding. The ‘soft landing’ where interest rates rise without forcing a recession looks more likely. But with rates likely to stay high for some time the risk has not gone away entirely. And high rates put stress on the whole financial system, which must be contended with.

For the United Kingdom the Bank of England has said that inflation is unlikely to return to its 2% target until the middle of 2025, setting up a prolonged period of high interest rates even as GDP growth, which was around 0.2% in the first half of this year, remains muted.

For many ordinary people the most visible sign of the economic strain is in house prices, which fell by 3.8% year-on-year in July. This is the fastest annual decline since 2009 according to Nationwide building society. Higher mortgage rates are reducing housing affordability and activity and are a source of risk for the broader economy.

We should note though that the UK FTSE All Share did rise by 2.6% in July, more than the 1.9% of large US companies. The FTSE 250, a measure of medium-sized companies, rose even more by 4.14%. This reflects the view that, whilst the UK may remain the worst-positioned of all rich countries in the current environment, the gap between it and the rest of the world is getting smaller as our inflation number starts to fall too.

In the US, the Federal Reserve delivered a 0.25% hike to push rates to 5.5%. Jerome Powell, the Federal Reserve Chair, stressed policy will remain restrictive until the Fed is confident inflation is durably coming down. June inflation of 3% (year-on-year) was below market forecasts.

Overall, though economic predictions improved somewhat over the month. The International Monetary Fund (IMF) raised its 2023 global growth forecast to 3.0% from 2.8%, citing economic resilience during the first half of 2023. Advanced economies face weaker manufacturing growth while Emerging markets could struggle with tight credit conditions which impose stress on their borrowing.

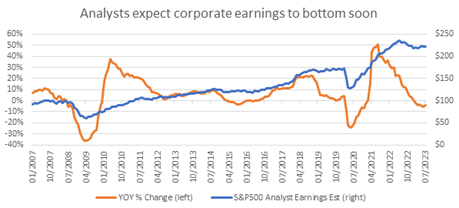

For investors one of the key considerations is how companies are coping with these challenging times. Many are finding it tough. In the United States so far earnings for the second quarter have fallen on average by 7.3% compared to last year. This is the largest decline since the pandemic.

Many companies are finding it tough but there were also some bright spots in technology and communications stocks. And there is real optimism that this may be as low as it gets for corporate earnings before the recovery commences.

Source – Bloomberg 01.2007 -07.2023

China’s growth challenges:

China’s economy stumbled in June with manufacturing surveys and retail sales growth missing forecasts. China’s retail sales grew 3.1%, slowing sharply from a 12.7% jump in May. While China is on track to hit its growth target of 5%, there are risks of the annual goal being missed for the second year in a row.

China’s property sector, which accounts for about a quarter of the economy, remains firmly in a downtrend, with new home prices for June stalling. Property investment slumped 10% in June year-on-year after a 16% drop in May. The ongoing slowdown in global manufacturing demand is having a significant impact on large parts of the economy and youth unemployment has increased significantly. Outbound shipments from the world’s second-largest economy slumped 12.4% year-on-year in June following a 7.5% drop in May. The need for urgent policy easing has so far produced limited policy intervention.

Conclusion:

The current environment is clearly mixed. There is plenty of evidence of a global economy in pain as a result of interest rate rises. However, the process of raising the cost of money, subduing demand, seeing inflation fall and then getting ready for an economic recovery is happening in an orderly and – in the scheme of things – quick fashion.

There is much cause to hope that earnings will improve in the second half of the year as the UK joins the rest of the rich world in bringing down inflation.

However, in times like this we should not simply move to the most risky assets to enjoy the recovery. We are deeply mindful of the fact that when rates are high much pain can be felt in markets as they await the recovery. So, we are acting with caution, gradually increasing our exposure to areas of the market that can benefit from recovery without taking undue risk.

We take much comfort that expected returns in fixed income remain attractive, particularly given our inflation forecast. We continue to favour large-cap quality and growth equities at this stage and will re-engage with more cyclical assets when inflation finally bottoms.

We remain confident that the opportunities available to us after two difficult years for markets are greater than they have been for many years and that we are well-positioned to capture the recovery for our clients.